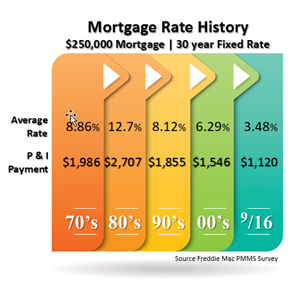

A quick tour of the Mortgage Market from the 1970" to Present! What was your first experience?

It’s not “if” the rate goes up but “when” the rate goes up; it could make a big difference for some buyers. Freddie Mac predicts that mortgage rates will be at 4.5% a year from now.

If buyers can afford a home with higher interest rates, it means higher payments. Higher payments might mean they won’t have the money to spend on other things like furniture or improvements to the home or an unrelated purchase like a new car.

When the rate moves 0.50% on a $250,000 mortgage, the payment goes up by $70.66 a month. If it moves 1.00%, the payment goes up by $143.74 per month, each and every month for the entire term of the mortgage which means paying over $50,000 more for the house.

The question facing every borrower in this situation is “How will you feel about having to pay more to live in the same house because you were not ready to commit?”

Then, there’s the borrower who is absolutely maxed out as to what they can qualify for or sometimes, it is a borrower who just refuses to pay a higher payment. When that’s the case, the buyer has to make a larger down payment. In the same example, a 0.50% increase in rate would require $14,873 more in down payment. That could make the purchase impossible or require the buyer to buy a lesser price home that will not have the same amenities.

Mortgage rates have been low for so long that some people think that is what they should be. There are some economists who believe that the economy will not be strong again until mortgage rates are in the 7% range.

To see how this type of scenario might affect you, go to the If the Rate Goes Up calculator.